OpenAI Wants Access to Your Bank Account.

May 27, 2026

On May 15, OpenAI launched bank account connectivity for ChatGPT Pro subscribers in the US - the $200/month tier. Via Plaid, it connects to 12,000+ financial institutions: Chase, Fidelity, Schwab, Robinhood, American Express, Capital One, and most others you'd recognize. Once linked, ChatGPT shows a unified dashboard of your spending, subscriptions, investment portfolio, and upcoming payments.

It's read-only, OpenAI says. ChatGPT can't move money. You can disconnect at any time, and your data is deleted within 30 days of removal.

Before I get into the privacy concerns - let's pause on who this is actually for. $200 a month is $2,400 a year. If someone is paying that to use ChatGPT, personal finance management is probably not their primary use case - it's a bonus feature on top of everything else they're already doing with the tool. That's a very different person from someone who downloads a budgeting app because they genuinely want to understand where their money goes.

For that second person - the one actually trying to build better financial habits - I want to explain why I think the "read-only" framing deserves more scrutiny than it's getting, and why Yavo deliberately takes a different approach.

Your Bank Data Is Not Like Other Data

When you let an app read your bank transactions, you're not sharing a preference or a habit. You're handing over a detailed record of your life.

Where you eat. Where you sleep when you travel. Which doctors you visit. What medications you might be buying. How much you spend on alcohol. Whether you're paying a therapist. Which political causes you donate to.

Bank statements reveal things about you that even your closest friends don't know. That's why the financial industry has strict regulations around this data - and why Plaid has faced significant regulatory scrutiny over how it handles the credentials and data it collects.

"Read-Only" Doesn't Mean Risk-Free

The read-only argument is real and worth taking seriously. ChatGPT can't initiate transfers or pay bills. That removes a significant category of risk.

But here's the part that gets glossed over: OpenAI doesn't connect to your bank directly. Plaid does. And Plaid has full read access - account numbers, balances, transaction history, everything. OpenAI saying "we don't see your full account numbers" may be technically accurate for their own systems. It says nothing about what Plaid sees, stores, or does with that data on their end.

You're not agreeing to one privacy policy. You're agreeing to at least two - and Plaid has its own history with regulators over exactly how it handles the credentials and data it collects during connections.

OpenAI's business is building AI models. Their terms of service give them wide latitude to use your interactions - including the context around them - to improve their systems. Your Fidelity portfolio and your Chase spending history are extraordinarily rich context. Even if that data never leaves their infrastructure, it shapes what financial products get surfaced to you, what the model assumes about people in your income bracket, and how future features get built.

And "deleted within 30 days" is a policy, not a technical guarantee. It means someone at the company decided to write that sentence. It doesn't mean every cache, log, embedding, or derived insight gets purged on day 31.

I'm not saying OpenAI or Plaid are acting in bad faith. I'm saying there are at least two parties with deep access to your most sensitive data - and that's worth understanding before you connect.

Why I Decided Not to Build Bank Connections into Yavo

When I was building Yavo, bank integration was on the table early. Plaid and similar providers make it technically simple. Most competing apps offer it. Users often ask for it.

I chose not to pursue it.

The reason is simple: I don't think the convenience is worth what you give up. To offer bank sync, I'd have to sign contracts with data providers, agree to their terms, and take on responsibility for how that data flows through a system I don't fully control. That's not a trade I'm comfortable making on your behalf.

Yavo doesn't see your bank data. It doesn't want to.

The Photo Approach Actually Works

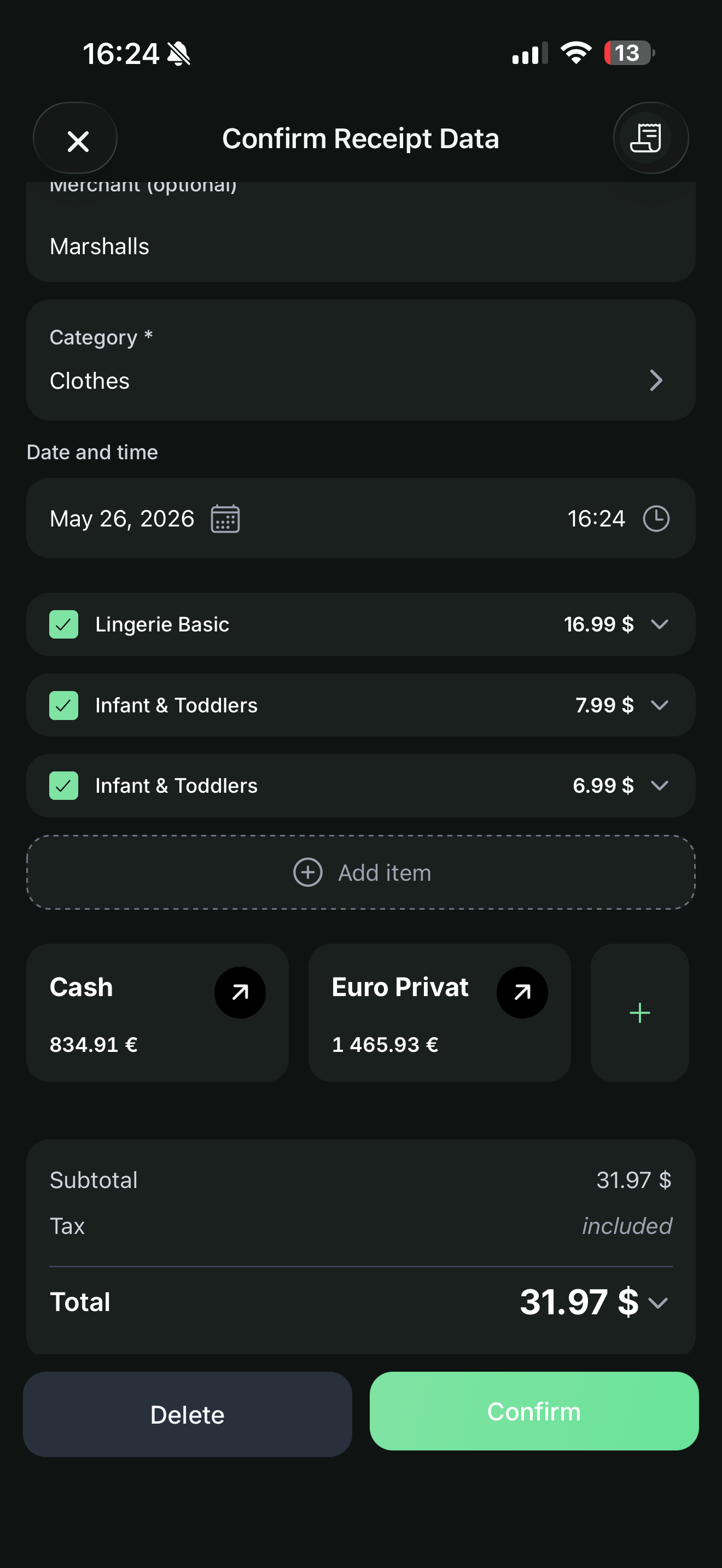

Here's what Yavo does instead: you take a photo.

A bank statement, a receipt, a bill - point your camera at it, and Yavo reads it, extracts the numbers, and adds the expenses automatically. The same result, without the data leaving your hands.

Yes, it takes an extra step. That's intentional.

Automation Isn't Always the Goal

There's a version of personal finance where everything is automatic. Your bank syncs, your transactions categorize themselves, your budget updates in real time. You never have to think about it.

I've heard people describe this as the dream. I think it's actually a problem.

The moment you stop looking at your expenses, you stop understanding them. The friction of manually logging a purchase - even a quick photo - is the moment you register that you spent money. That awareness is the whole point.

Budgeting apps that sync everything automatically often show users a perfect dashboard that they check once and forget. The habit never forms because the effort never exists.

With Yavo, you're involved. You take the photo. You see the number. You know what's happening with your money.

What You Should Ask Before Connecting Your Bank to Anything

If you're considering linking your bank account to any AI product - not just OpenAI - ask these questions first:

- Who actually holds my credentials or tokens - the app, or a third-party intermediary like Plaid?

- Will my transaction history be used to train models?

- Can I delete my data, and is that deletion actually permanent?

- What happens to my data if the company is acquired or goes bankrupt?

- Is the convenience worth the permanent transfer of this information?

These aren't paranoid questions. They're basic due diligence for data this sensitive.

Is This the End of Budgeting Apps?

The second debate running alongside the privacy one is whether ChatGPT just made standalone expense trackers obsolete. If the most powerful AI in the world can now see all your accounts and answer financial questions in plain English, why would you use a separate app?

I think this misreads what budgeting actually requires.

Seeing your data summarized is easy. Changing your behavior is hard. ChatGPT showing you that you spent $800 on dining last month is useful once. An app you actively use - one where you take a photo of a receipt, review a category, and feel the small friction of logging - builds a habit. That habit is the thing that changes your finances.

The feature that makes ChatGPT's integration impressive (it's automatic, it's passive, you don't have to do anything) is the same feature that makes it unlikely to change how you spend. Awareness without involvement rarely leads to action.

Budgeting apps that survive this moment won't be the ones that compete with ChatGPT on AI. They'll be the ones that understand why friction matters.

The Bottom Line

OpenAI connecting to bank accounts is a product decision that prioritizes convenience. I understand the appeal. But your financial data is not a reasonable price to pay for a slightly more automated budget dashboard.

Yavo gives you AI-powered expense tracking without ever touching your bank account. Take a photo of anything - a receipt, a statement, a bill - and it's in your records, categorized, and ready for reporting.

Your money stays between you and your bank.

Track your expenses with Yavo - free to download